One of the top criteria that lenders look at when making a mortgage loans decision in the United States is stable income. Banks and lenders wish for borrowers to be able to return their loans on schedule without hassles. When the lender is assured that monthly payments will be kept up, he or she will have the confidence needed to provide you with a regular income.

When it comes to financing, whether they’re looking into a mortgage, a car Loans , a personal loan, or a credit card, income stability is a huge factor in the end. If you are able to work consistently, you will find that you qualify for better loan terms and lower interest rates will be offered.

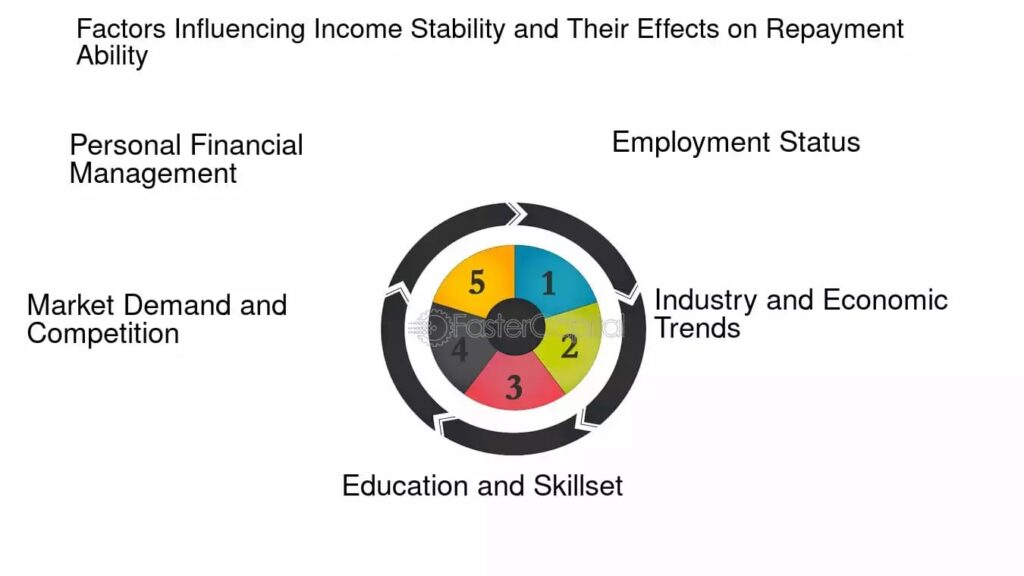

This article explores the significance of stable income for loans in the United States and its impact on loan approval, repayment capacity, and financial stability.

Lenders Want Proof of Financial Stability

Lenders make every effort to minimize financial risk prior to loan approval. Stable income indicates that a borrower can pay debts responsibly for a long-term period. Someone that has regular income would be more reliable than someone who does not.Lenders may consider the following when making decisions on loan applications:

- Monthly or yearly income

- Employment history

- Job stability

- Existing financial obligations

- Future earning potential

Those who have a regular source of income and steady employment will find it easier to get loan approvals. However, borrowers who do not have regular work could be subject to more stringent requirements or requirements to present more paperwork.

When Your Income is Steady, Your Chances of Getting a Loan are Improved

If you have a steady income, you are likely to receive loan approval more easily. A regular income means that lenders can feel more secure to provide the money because you are likely to be able to repay the loan.For instance, someone working full time for a number of years may be more likely to be able to qualify than a person who switches jobs often.

When a lender sees the income that is stable, and that payment is going to be made every month, it gives them a feeling of stability, which is what they want. Stable income allows a lender to feel safe about the monthly loan payments being made without a problem. Depending on the borrower, they may also be eligible for more loan. These lenders might be allowed a bigger loan by banks due to their financial responsibility. Stable income is particularly critical when lending money, specifically when it comes to a mortgage loan, where the lender wishes to know that they will be able to recoup their loan over many years to come.

Stable Income could be used to Lower Interest Rates

Having a stable income can also increase the likelihood of loan approval and can lead to better interest rates. Financial stability is a sign of lower risk for lenders, so they will be more inclined to give loans to stable borrowers. Having a lower rate can lower monthly payments and save borrowers a lot of money over time. Even a miniscule disparity in rates can add up, particularly when it comes to home loans and business financing. Lenders are likely to provide better terms to borrowers with stable financial history and a steady income and a long term employment.

However, those with inconsistent income might qualify for a higher interest rate due to increased risk.A sound financial position will also enable borrowers to have more leverage in speculating on loan offers from various banks and lenders.

Type of Employment also Influences the Decision on Loan

The nature of the borrower’s job may affect the assessment of income stability. The income of a full-time employee is more predictable and steady, thus making him or her a safer borrower for the lender.People who work part-time, freelance or are self-employed might be subject to further checks as their earnings fluctuate from month-to-month. But it does not imply they can’t be qualified for the loans properly.

For the self-employed, they typically must furnish:

- Tax returns

- Bank statements

- Business income records

- Profit & Loss statements

- Evidence of regular income

Lenders want to see it’s been consistent over time. Keeping good financial records will give the lenders more confidence in the freelancer/business owner and increase the likelihood of an approval.

Stable Income Makes it Easier for Borrowers to Handle the Debt

Steady wage is advantageous to the bank, as well as the borrower. Visit wage permits people to more effectively pay bills and diminish monetary stretch. A tried and true salary can empower borrowers to bargain with month to month bills and unanticipated events. The borrower can make convenient installments and have a positive credit score if they have a relentless wage.

When you are late with your installments, it can contrarily affect your credit rating and lead to budgetary challenges afterward on. Individuals who have a relentless wage stream can create sensible budgets and longer-term financial plans . This will allow them to not take on more debt than they have the funds to pay back. People who have irregular income might not be able to cope during the low income level. Financial instability may also make it hard to manage debt responsibilities and make it more likely that you will not be able to make payments.

Credit Score and Stable Income Work Together

During the mortgage loan application, one’s credit rating and steady earnings go hand in hand. A good credit rating indicates responsible financial practices and steady earnings indicate the capacity to pay back.

Lenders usually review:

- Payment history

- Existing debts

- Credit card usage

- Income consistency

- Employment records

If the borrower has a good credit history and a steady income, he or she will be more likely to get a quick approval and the best loan terms. Those who have an average credit score could benefit from demonstrating a positive financial history as evidence of financial stability.This pairing also puts you at a higher risk of being approved for higher loans, particularly those you are applying for to purchase a business or home.

Conclusion

A steady income is a major factor in loan denials in America. Lenders want to be assured that borrowers will be able to meet loan obligations without major financial hardships. Those who have a reliable income have more chances of being approved for loans, pay lower rates of interest and better conditions when repaying. Debt management is also easier because of stable income, which enables borrowers to keep their financial habits in check.

While freelancers and self-employed people may encounter additional scrutiny, having good finances can still benefit them in getting a successful pass.Ultimately, it is the stable income that brings security to both lenders and borrowers. When coupled with sound credit and prudent financial management, it can significantly enhance the availability of low-cost loan opportunities in the USA.